COVID ECONOMIC CRISIS:

A BETTER WAY OUT

The European Union’s €750 billion Covid recovery package presents a once-in-a-generation opportunity to transform our economy.

As the window opens, however, the EU is still relying on discredited, short-termist economic theories that will leave us vulnerable to accelerating climate change and falling living standards, while Member States plan to waste a huge portion of the recovery package rebuilding an unsustainable economy.

Europe must seize this chance to build a bridge to a new economy that is sustainable, resilient, and guarantees better living standards for everyone. Join our call for European Finance Ministers to rethink the recovery.

Sign Our Call

Environmental Sustainability

Climate change threatens us all, bringing huge environmental disruption. To mitigate this, the EU must urgently invest in sustainable industries and technologies to meet the Paris Agreement emissions targets and avoid environmental disaster.

While Covid-19 ravaged Europe, global carbon emissions in 2020 dropped by 8%, the first overall decline since the Industrial Revolution. One year isn’t enough, as we need the same percentage fall in emissions levels every single year until 2030 to meet our Paris Agreement targets. If we rebuild the pre-pandemic economy, we could see a catastrophic 4.8°C rise in average temperatures by the end of this century. As the world’s largest trading bloc, Europe plays a critical leadership role in upholding the Paris Agreement and fighting climate change.

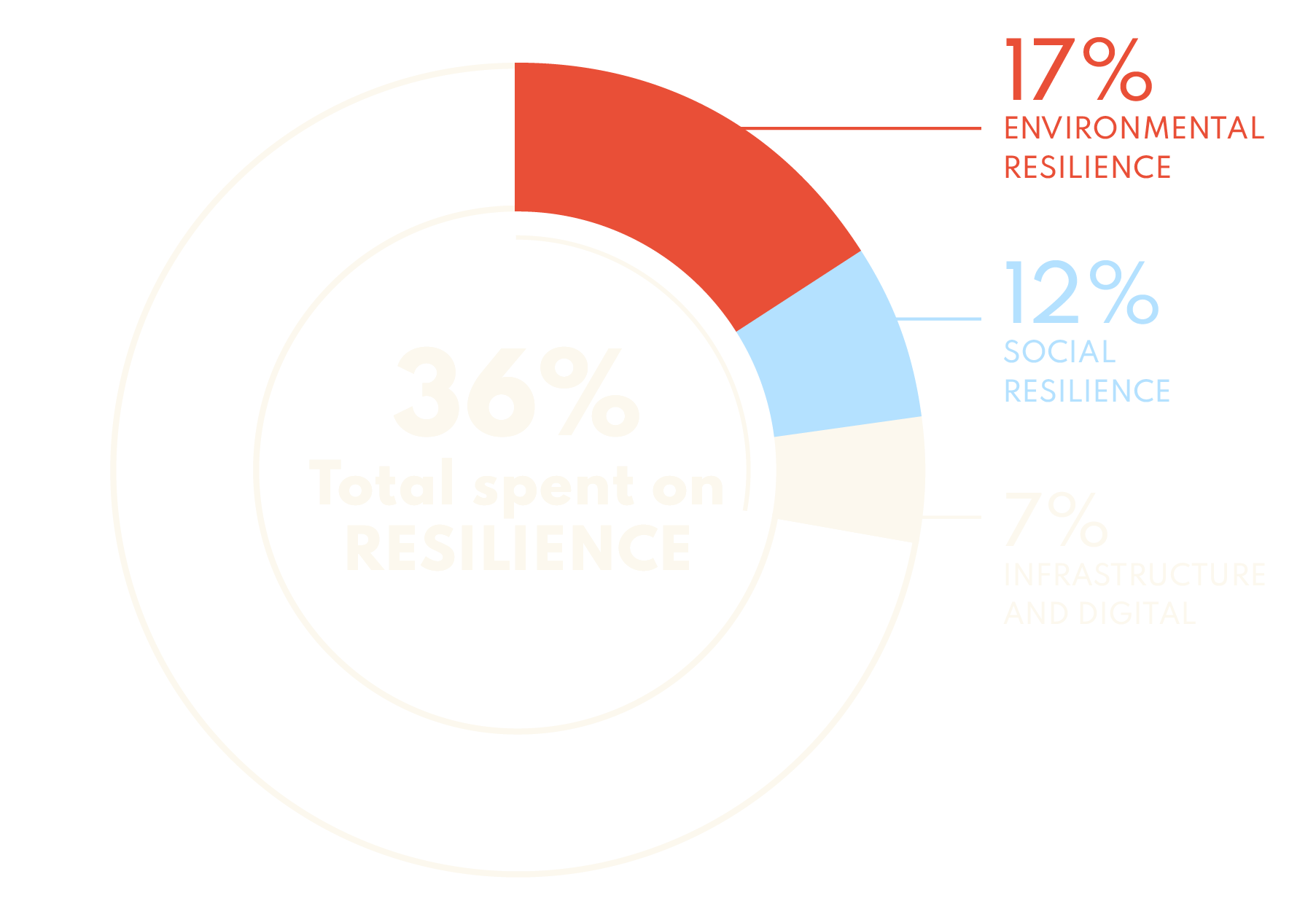

Current spending plans: falling short

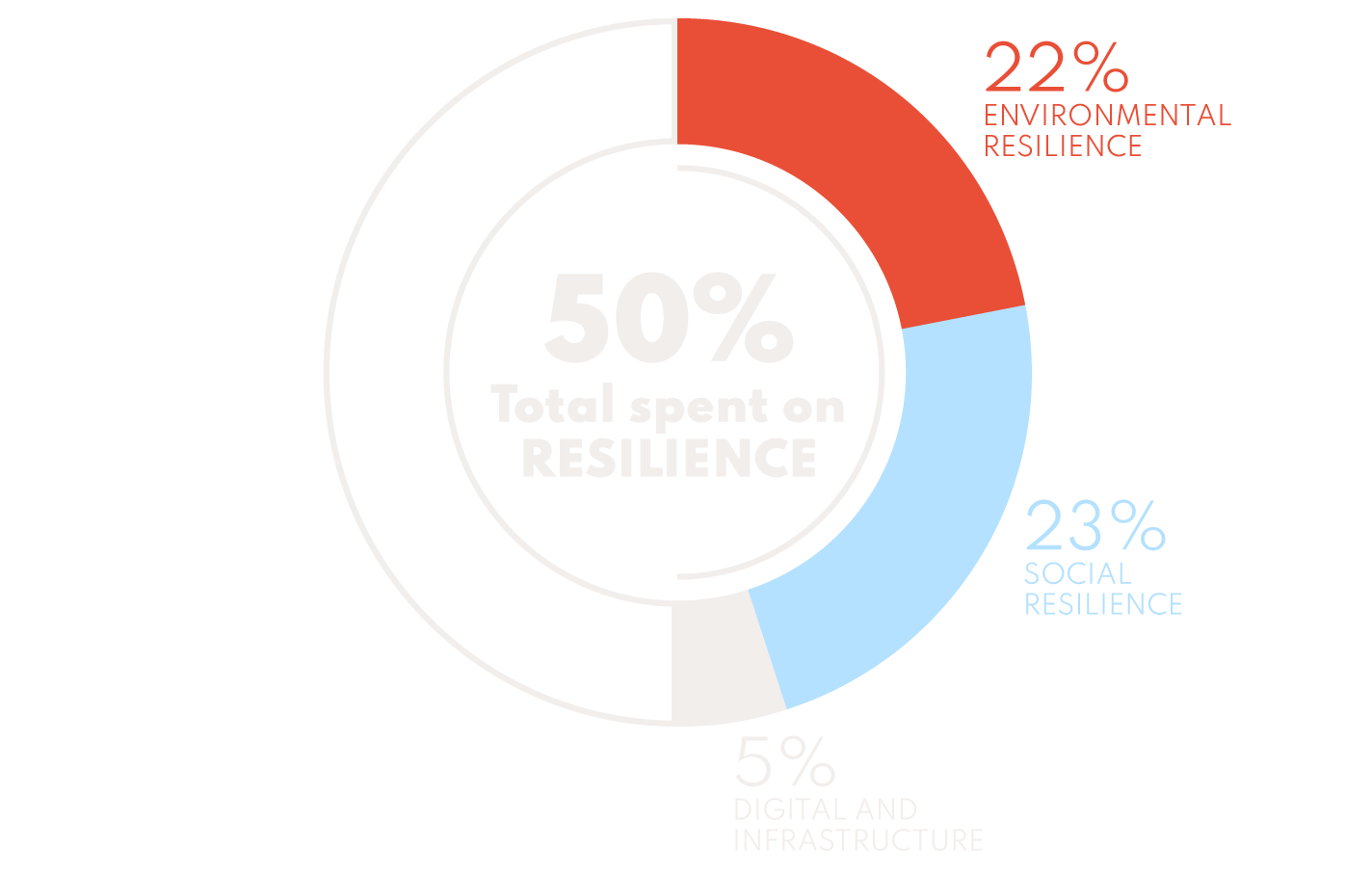

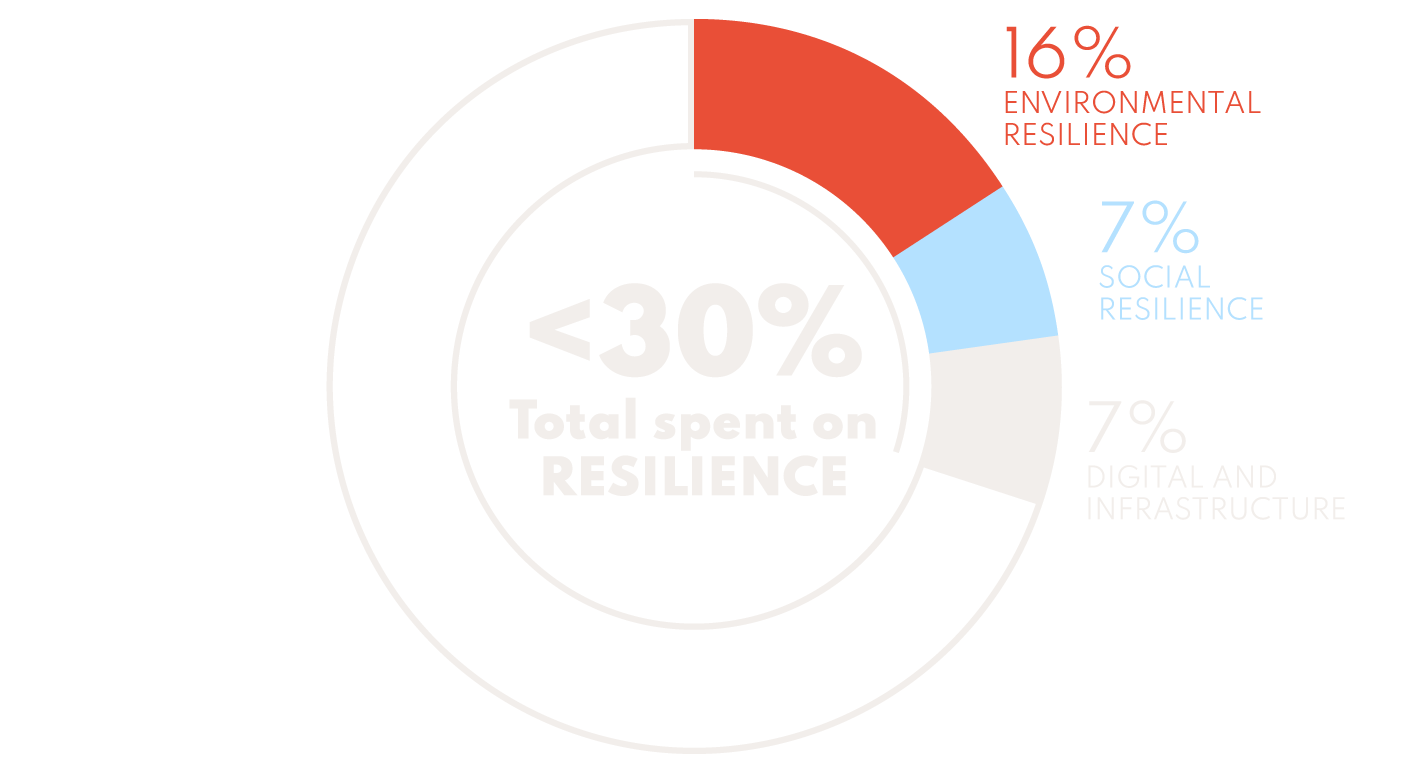

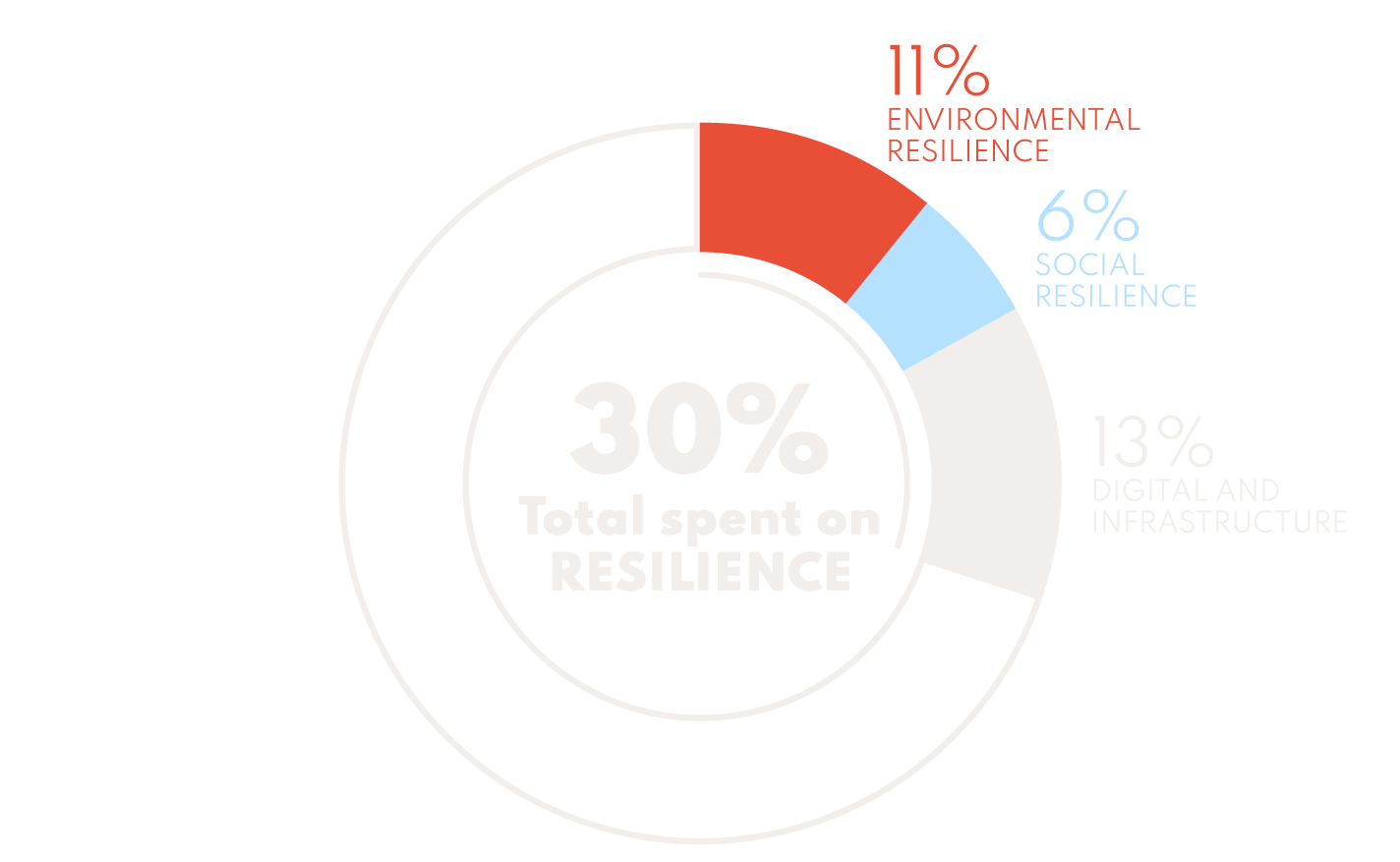

In current recovery spending plans, Europe’s largest economies fall short on environmental resilience. France has allocated only 22% of its €100 billion budget to it, Germany just 16% of €130 billion, while Spain has earmarked a meagre 11% of €72 billion.

The spending gap: pandemic recovery package not enough

The EU Commission spelled out the need to invest €470 billion every single year until 2030 for Europe to meet its environmental objectives, including the Paris Agreement emissions targets. The pandemic recovery plans take a step in the right direction, but we need a much more ambitious long-term path.

What needs to happen: build a sustainable future

Chasing economic growth at any cost is dangerous and short-sighted when the future sustainability of the planet is at stake. There is also no credible evidence that private financial markets alone can tackle climate change. These are by nature risk-averse and driven by short-term profit, so the EU cannot rely on them to plug the financing gap. We need to unlock public finance through a reform of the EU fiscal framework in order to bridge the green funding gap.

Europe’s Finance Ministers must change their course and end support for industries that won’t shift to sustainable business models. Instead, support those that can, and finance the development of new sustainable activities.

Social Inclusion

Hundreds of thousands of Europeans have lost their lives to coronavirus, the ranks of the jobless swell into the millions while the economy has shrunk by almost 8%. It didn’t have to be this way. If governments had spent just €4 per person preparing for a pandemic, this catastrophe could have been avoided.

The pandemic has shown how decades of short-term thinking and spending cuts for vital public goods like hospital beds, doctors and nurses have left our society vulnerable to crisis.

Current spending plans: Social resilience takes a hit

In the current recovery spending plans, France has allocated only 23% of its €100 billion budget to social resilience, while Germany has allocated just 7% of €130 billion, Spain only 6% of €72 billion.

The spending gap: Social infrastructure outlays fall short

Europe cannot return to the pre-pandemic status quo of stagnant living standards and household incomes. In many parts of Europe, unemployment remains higher than before the 2008 Global Financial Crisis. Nearly one in five Europeans are currently at risk of poverty, and 5% suffer from severe material deprivation. An independent expert group appointed by the European Commission also identified a social infrastructure investment gap of at least €142 billion per year, in physical facilities like hospitals, schools, and social housing.

What needs to happen

For too long, European Finance Ministers have prioritised meeting short-term deficit reduction objectives above the social needs of European citizens. With constraints on public spending, calls mount for the private sector to fill the social spending gap. But social infrastructure and services are not meant to be run for profit, and the private sector running public services like healthcare can often narrow equal access. This undermines the goal of long-term social resilience.

We need a socially just transition that supports workers to retrain for the green jobs of the future, and guarantees a decent standard of living for everyone. And we need proper public investment in infrastructure such as hospitals, schools and social housing, and services like healthcare, education, welfare support and skills training.

Sign our call to European Finance Ministers

Join us as we call on Europe’s Finance Ministers to rethink the recovery and build a new economy that is sustainable, resilient and leads to higher living standards.

Dear Finance Minister,

The Covid pandemic has forced Europe to temporarily lift its public spending limits to allow for a historical public stimulus. This is the perfect moment to invest into a green and social transition. Yet, the amounts invested into the so-called recovery of yesterday’s unsustainable economy eclipse the amounts pledged to building a resilient future economy.

This misallocation proves that, despite compelling lessons from the Covid crisis about the importance of long-term planning and investment in resilience, we are still prioritising short-termist economic indicators – the growth of any activity, even if it is harmful – over long-term sustainability. If we waste these once-in-a-generation public stimuli, we obstruct a most-needed transition and set Europe on a tragic path towards further climate change and social disruption.

We request you to review these recovery plans. In doing so, the plans must:

- End support for unsustainable activities that cannot be made sustainable.

- Support people and workers whatever it takes: guarantee living standards for all, and ensure a just transition.

- Invest in the green transition and lay the foundations for an economy based on a resilient production and consumption system.

We also call you to weigh in the debate to change the EU rules for public spending:

- Avoid a return to austerity, as recommended by chief economists at the OECD and the IMF.

- Reform the fiscal framework to put environmental and social goals at the heart of EU economic governance.

We must stop using unfounded economic numerical indicators such as the debt-to-GDP ratio, and put an end to imposing short-sighted reforms to assess and allow public expenses. Instead, responsible fiscal policy should aim at progress towards wellbeing and resilience measured, among others, by indicators such as CO2 emissions, precarity and inequality.

Signed,

...

Expand letter Sign letterOUR FIVE POINT PLAN

1. End support for unsustainable activities

Recovery financing must not be spent on supporting the fossil fuel industry and other unsustainable activities that have no place in the green economy of the future.

Why?

Support must be stopped for unsustainable activities in industries that cannot transition to more sustainable models, such as fossil fuel companies. Supporting these industries will bring a three-pronged, long-term economic loss. This stems from multiplier effects of: supporting industries that cause additional global warming and environmental disruption; the opportunity cost of failing to invest in sustainable industries; and finally from job losses and stranded assets when these businesses are inevitably forced to wind up. Such spending would be irresponsible.

The European Union must use its own definitions of sustainable spending outlined in the Taxonomy Regulation to assess spending plans, end support for industries that cannot transition to more sustainable business models, support those that can do so, and actively finance the development of new sustainable activities.

2. Guarantee living standards for all

Europe must ensure spending plans play an active role in guaranteeing a decent standard of living for everyone, through direct support for all who need it during the recovery and beyond.

Why?

Workers across Europe have suffered for decades from stagnant, and in some cases even falling, household incomes and living standards. The European Union also suffers from a range of social issues that require long-term public spending.

Some countries in Europe still face higher unemployment rates than before the Global Financial Crisis, and the pandemic may also bring about long-term unemployment for millions unless action is taken, with levels already having risen to 8.1% in 2020 and expected to rise further. Compounding this, there is a €142-plus billion per year social infrastructure investment gap identified by experts appointed by the EU Commission. Those investments improve “hard” facilities like hospitals, schools, and social housing.

Jobs losses will be inevitable in unsustainable sectors that we need to phase out. European Member States must ensure that during the transition to a more resilient economy, people’s basic needs are met and that human dignity is assured through a guaranteed income, and offer retraining to those who need it. This must be guaranteed no matter the cost. And we need proper public investment in hospitals, schools and social housing.

3. Invest in the green transition

Europe must embark on a programme of ambitious spending to build the sustainable economy of the future, including green energy production, sustainable transport infrastructure, energy efficient buildings, environmentally friendly agriculture, and biodiversity protection.

Why?

Private actors do not plan for the future, nor do they account for “externalities” - such as ecological damage and greenhouse gas emissions - resulting from their activities.

Improving environmental regulation and transparency about the environmental impact of their economic activities may help to reduce some damages. But it will fall short of transforming the modus operandi of these actors, be it risk aversion or short-term profit-seeking.

Some of the necessary activities to transition to a sustainable and resilient society are risky, not profitable, and require long-term investment. That is why we need governments to embrace a long-term vision backed by public spending to invest in these riskier sustainable ventures where private actors likely will not.

4. No return to austerity

Europe must reform fiscal rules limiting borrowing when deficits reach greater than 3% and the debt-to-GDP ratio is higher than 60%. The return to fiscal austerity must be avoided.

Why?

Many EU Member States will face a deficit of almost 6% of gross domestic product and a debt-to-GDP ratio of around 100% in 2021. Unless European fiscal rules are reformed, this means a return to austerity that will bring further economic damage, hampering the recovery and reversing any progress on environmental and social resilience.

Structured around the assumption that public deficits are always bad, the European fiscal framework requires that countries should strive to achieve structurally balanced budgets at all times. Austerity is the medicine that kills the patient. In the aftermath of the Global Financial Crisis, austerity had a devastating effect in countries like Greece, where its economy shrank by 25% and unemployment rose by the same proportion.

The world’s most senior economists at the International Monetary Fund and the Organisation for Economic and Cooperation and Development now promote fiscal activism instead of austerity. They recognise that the public purse is not the same as a household credit card, and that serious economic damage can be caused by tightening the purse strings too soon after a crisis. The state must play a crucial role in stabilizing the economy after an economic shock to avoid the knock-on effects of rising unemployment and falling consumption, which can spiral into a deep economic crisis.

We must no longer follow the outdated economic orthodoxy to “balance the books” whatever the context. This short-term thinking overlooks the future economic shocks we face by failing to take appropriate action now. Balancing our books in the long term requires that we spend now to ward off shocks in the future, and invest to build an economy that is resilient to climate change, pandemics, and social crises.

5. Reform the European fiscal framework

The European fiscal framework must be reformed to prioritise long-term environmental and social resilience over short-term fiscal sustainability.

Why?

The new economic consensus recognises that borrowing to invest in the future is one of the most powerful tools at a government’s disposal, bringing long-term benefits and future prosperity. While current recovery spending provides a welcome break from the EU logic of balanced books, there needs to be a permanent revision of the European fiscal framework.

Fiscal policy should move on from the current obsession with the quantity of public spending to an increased focus on its quality. We should cast aside adhering to arbitrary numerical thresholds such as the 60% debt-to-GDP ratio, and instead focus on concrete measures of progress towards wellbeing and sustainability, such as greenhouse gas emissions reductions and falling inequality levels. This approach falls in line with the latest thinking from chief economists of the OECD and the IMF.

Inflation remains stubbornly low and governments face low or even negative borrowing costs. Given this, we now have an opportune moment for the Member States of the European Union to borrow funds to invest in a sustainable and socially inclusive transition to a resilient future economy.

HOW DO THESE COUNTRIES SCORE?

Select a country from this list to see how their spending plans score for environmental and social resilience:

Overview

Of the 302 Billion Aggregate Spending of Germany, France and Spain:

Download our summary analysis

ABOUT

Rethink the Recovery is a campaign coordinated by Finance Watch, made possible with the help of the partners listed below. We are a diverse coalition of non-profit organisations, consumer groups, trade unions and think tanks. The campaign’s aims are twofold: to embed resilience within the heart of the recovery plans and to reform the EU fiscal framework. We believe that we now have a once-in-a-generation opportunity to transform our economy.

What is Rethink the Recovery?

Rethink the Recovery is a civil society campaign advocating for resilient recovery plans and a reform of the EU fiscal rules. We believe that civil society needs to come together to tackle this crucial topic. This campaign aims to contribute to building a network of activists and economists that want to advocate for a reform of the fiscal rules of the European Union.

Who should sign the call?

Anyone who supports our message can sign the call. In particular, we want to gather as much support from civil society as possible, including environmentalists who are fighting climate change, trade unionists fighting for better wages and improved living standards for workers, and economists working in a university or think tank.

We encourage all citizens and activists concerned about climate change, social and tax justice, and sustainable economics to join!

How can I support the campaign?

You can support the campaign by signing the call, sending it to your colleagues or friends, and sharing the campaign on social media. If you represent an organisation or group, please read the section below on how to become a partner.

How can I become a partner?

If you want to become a partner of the campaign, please send an email to contact@rethinktherecovery.org and we will get in touch with you shortly. As a partner, your logo and your own research on the recovery plans or fiscal rules will be displayed on the website. You will also get access to unbranded social media assets (including graphics and videos), that you are free to modify and use for your own communication.

What happens with my signature?

Your name will be displayed on the letter that we will handover to EU Finance Ministers in May. We will update you about campaign developments, and send you material to learn about the EU fiscal rules and how to reform them. You can always unsubscribe from our emails, of course. Read our privacy policy for details.

When will the Finance Ministers receive the letter?

We will hand over the letter to EU Finance Ministers in May - one month before the EU Heads of State Summit on 24-25 June.

When will governments have to submit their recovery plans to the EU?

Until 30 April 2021, governments have to submit their recovery plans, called National Recovery and Resilience Plans (NRRPs), to the EU Commission. The NRRPs are a small part of the national recovery plans that we have analysed. If the EU Commission agrees with the measures proposed in their plans, governments can receive partial funding for their measures through the €672.5 billion EU Recovery and Resilience Facility. Some of the NRRPs, like the Spanish one, are fully EU funded.

What is the EU fiscal framework?

The EU Fiscal Framework is a complex architecture composed of a set of rules constraining Member States’ fiscal policy, intertwined with a system of governance aimed at enforcing these rules. It reinforces short-term focused fiscal policy and prevents us from reaching our social and environmental goals. Without reform it could break the economic recovery.

For more information, read Why and how to reform the fiscal framework?

How did you conduct your analysis?

The analysis of the recovery plans assesses the measures in two ways: their environmental and social sustainability, as well as their orientation towards recovery versus resilience. Resilience measures were defined to be long-term oriented and expected to have transformative economic effects beyond 2021 (up until 2030-2050). Recovery-oriented measures were defined as dictated by the urgency of the pandemic crisis response and aimed at the restoration of the pre-crisis economy.

For more information, please refer to our Methodology Factsheet and Analysis Matrix, or write to contact@rethinktherecovery.org.

I have further research on this topic to share, who should I send it to?

Please send your research on the recovery plans of any European Member State to contact@rethinktherecovery.org. If you decide to become a partner of the campaign, we will display this research on our campaign website.

Who can I contact with any questions?

For any further questions, please don't hesitate to write to contact@rethinktherecovery.org.

Why is this important now?

It's important that we get our message to European Finance Ministers in May, because Finance Ministers and Heads of States will make key decisions on the recovery and fiscal rules in June.

Additionally, there is legislative momentum around reforming the European fiscal rules. Together with a growing agreement among experts for a reform of these rules, a concerted push by civil society is needed to make sure these new rules enable instead of hinder a much needed economic transformation.

Read more about why it’s the right time for a reform of the fiscal rules in Why and how to reform the fiscal framework?